✉ info@lettuce.africa ☏ +27(87)-265-1233 ✆ +27(76)-616-9141 ⚐ Bryanston, Johannesburg Mon - Sat ( 9am : 5pm )

How It Works.

Get Started:

| Step 1: Decide how much money you need and when you want to repay it. |

Step 2: Complete our secure online application form. |

| Step 3: We verify your income. Once your loan has been approved, we will need to verify your income. You will need to provide us with your most recent payslip or bank statement which clearly shows your personal details as well as your income. Once verified, we will send you a pre-loan agreement to sign as required by the National Credit Act. Once we receive your signed agreement we will send you a debit order consent authorisation for the agreed repayment amount. |

| Step 4: The money is transferred to your bank account. The loan amount is electronically transfered to your bank account. We will collect repayment from your bank account on the due date, so you just need to ensure the required funds are available. |

Lettuce Loans ® is a division of Union Avenue ® Financial Services (Pty) Ltd, a Registered Credit Provider, NCRCP18518.

National Credit Act Disclosures

| A credit agreement must not require payment by the consumer of any money or other consideration, except the principal debt and additional costs permissible in law. The National Credit Act, (NCA) in section 101, prescribes those permitted costs in addition to the principal debt as described below. |

The Initiation Fee The initiation fee is a fee that the credit provider charges the consumer for entering into a credit agreement. The consumer is only liable to pay initiation fee if he/she finally concluded the credit agreement. The consumer must be given the option of either paying the initiation fee separately up front with no interest incurred, or paying it off in instalments together with the capital repayment, in which case interest will be charged on the initiation fee. The Act regulates initiation fees by specifying the maximum initiation fee that consumers may be charged. The maximum initiation fee is R165 for the first R1000, plus 10% of the amount over R1000, but never to exceed R1 050 or 15% of the principal debt. |

The Service Fee A service fee is a fee that a credit provider charges a consumer for administering or maintaining the credit agreement between them. This fee can be charged monthly, annually or on a transaction basis. The National Credit Regulations provide that the credit provider can charge the consumer a service fee to a maximum of R69.00 a month or a maximum of R1,020.00 per year if the consumer pays an annual service fee. If the credit agreement is settled sooner than originally agreed by the consumer and within the year to which the annual service fee relates, the credit provider must refund the unused portion of the service fee to the consumer. |

The Interest Rate Interest is the amount that a credit provider charges a consumer on the outstanding balance of a credit agreement. Interest is calculated using a percentage which is called the interest rate. The interest rate must be reflected on the credit agreement that the consumer signed at the time of entering into a credit agreement. The Act regulates interest rates by providing maximum interest rates that credit providers may charge consumers for various credit agreements. These rates are linked to the Repo Rate (Repurchase Rate), which is the official rate at which banks borrow money from the South African Reserve Bank. |

Credit insurance Credit insurance may be required by the credit provider when a consumer takes up a credit product. This insurance will then cover the debt due to the credit provider if the insurance is called up because of a default in payment. The Act stipulates that the insurance cover may not exceed the obligation outstanding to the credit provider. As such, the insurance cover must decrease as the outstanding balance due to the credit provider decreases. The consumer may not be forced to take the insurance offered by the credit provider if they elect to utilise an insurance policy of their choice. When the consumer chooses to use their own insurance, the credit provider can request that the credit provider pay the insurance premiums and, after that, bill the consumer every month. All insurance premiums payable to the credit provider must be by way of monthly premiums, except in the case of a significant credit agreement where an annual premium may be recovered at the beginning of each credit agreement period. |

Lettuce Loans ® is a division of Union Avenue ® Financial Services (Pty) Ltd, a Registered Credit Provider, NCRCP18518.

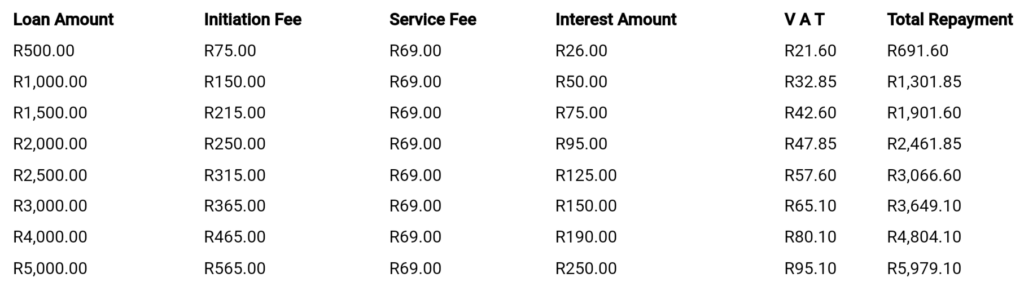

Illustrative Rates & Fees

* The table above is illustrative only, based on a one (1) month loan.